AI company Anthropic has announced that its unreleased model, Claude Mythos Preview, has discovered previously unknown mathematical weaknesses in cryptographic algorithms that human researchers had missed for years.

Cryptography uses sophisticated algorithms to protect web traffic, email, software updates and sensitive information like banking details. It does this by rendering the data completely unreadable.

The Anthropic team describes its work in two papers.

For decades, getting to space has largely meant one thing: launching vertically atop massive rockets from fixed launch pads. But what if the future of space access also includes aircraft capable of flying at more than twice the speed of sound, launching payloads from the edge of the atmosphere, and providing researchers with affordable access to hypersonic flight and microgravity?

Joining us today is Tim Franta, Chief Executive Officer of Starfighters Space (https://starfightersspace.com/), an aerospace company operating the world’s only commercial fleet of flight-ready Mach 2+ F-104 Starfighters. Based at NASA’s Kennedy Space Center, the company is building capabilities that span hypersonic flight testing, airborne research, astronaut and pilot training, and an ambitious air-launch platform known as STARLAUNCH, designed to provide more flexible and responsive access to space.

Tim brings an unusual blend of aerospace leadership, public policy, infrastructure development, and strategic finance. Before leading Starfighters Space, he helped shape Florida’s modern space ecosystem through leadership roles with Energy Florida and the Florida Space Authority, where he worked on launch infrastructure, legislation, and hundreds of millions of dollars in space-related investment.

Today we’ll discuss why aircraft may become an increasingly important part of the space economy, how commercial innovation is changing access to orbit, the growing importance of hypersonic technologies, and what the next decade of aerospace infrastructure might look like.

The Iranian state-backed hacking group tracked as Nimbus Manticore (aka GalaxyGato, Mirage Kitten, Smoke Sandstorm, Subtle Snail, and UNC1549) has been attributed to a fresh set of attacks targeting entities across the Middle East, Africa, and South Asia.

The intrusions involve the use of a previously undocumented Windows backdoor called NightLedger and two custom WebSocket tunnelers, BridgeHead and ArcBridge, with an aim to maintain covert access.

Targets of the campaign include Egypt, SMB and government environments in Jordan and Tanzania, aviation organizations in Pakistan, telecommunication companies in Ethiopia, and financial-sector entities in Burkina Faso, per Kaspersky.

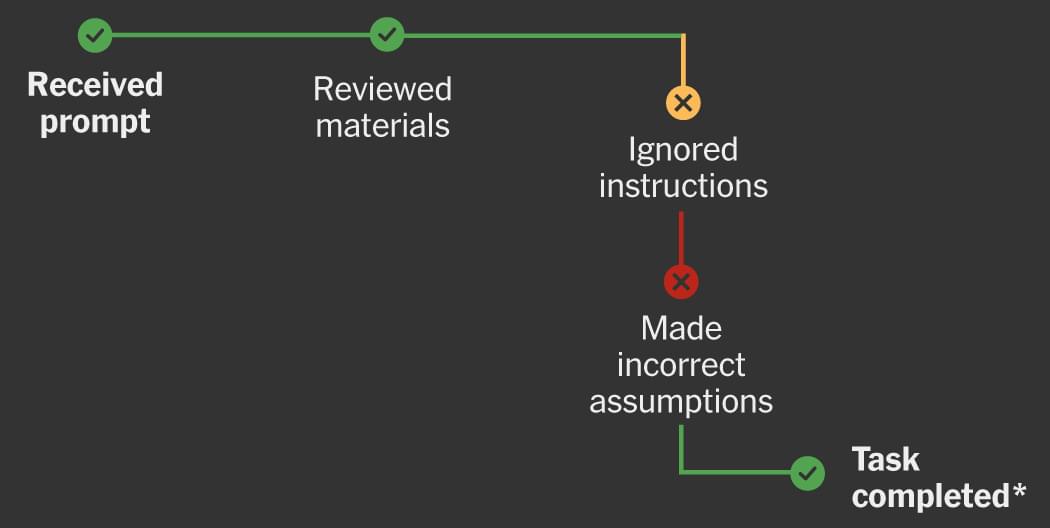

We gave an A.I. tool full access to a laptop with pre-configured apps and sought to answer a simple question: Can artificial intelligence do an office job?

Some corporate executives seem to believe it can. More than 200 tech companies have cut roughly 120,000 jobs this year, according to Layoffs.fyi, an industry tracking site; Meta, Oracle and others have all recently made substantial cuts to their work forces, citing A.I. as the driving force; and after laying off about 1,100 employees, the chief executive of Cloudflare said recently that he expected A.I. to replace workers in middle management, finance and marketing.

In our experiment, we deployed A.I. “agents” to act as office workers and found that they were capable of performing some of the tasks we assigned, but not all of them. The agents, which can act autonomously and make decisions based on detailed instructions, excelled at problems they could solve by writing computer programs. But they struggled with understanding the nuances of human language and at navigating user interfaces like the Chrome web browser.

Hackers are changing the DNS settings on Wi-Fi devices at hotels and conference centers to redirect users to fake Microsoft 365 login pages.

The campaign has been ongoing since at least June and impacts organizations in various sectors, including financial services, professional services, legal, health care, energy, and retail.

Cybersecurity company ReliaQuest identified compromised Wi-Fi gateways in multiple U.S. cities as well as other regions of the world, such as India and Saudi Arabia.

Discover how original Yamanaka co-author Dr. Koji Tanabe uses automated iPSC cassettes and autologous stem cell secretomes to reverse cellular aging and repair damaged joints.

Some links are affiliate links so we will earn a commission when they are used to purchase products.

In this landmark episode of Modern Healthspan, we sit down with Dr. Koji Tanabe, founder and CEO of iPS, Inc. and co-author of the historic 2007 Nobel Prize-winning paper on human-induced pluripotent stem cells (iPSCs). Dr. Tanabe shares how twenty years of technological advancement have raised iPSC reprogramming efficiency from under 1% to over 80%, while cutting manufacturing costs through automated cleanroom cassettes. We discuss practical longevity applications available today, including autologous stem cell banking from a simple blood draw, secretome extract therapies for joint and skin rejuvenation, and Japan’s approval of iPSC-derived heart tissue. Finally, Dr. Tanabe offers a critical scientific perspective on in vivo partial reprogramming, detailing the cellular identity loss and tumor risks associated with OSK gene delivery. Watch now to learn where stem cell age reversal truly stands today.

📚 Chapters. 00:00 — How the 2007 Yamanaka Breakthrough Reverses Cell Age. 09:58 — Cellular Reprogramming in Nature (Salamanders & Limbs) 15:01 — From 1% to 90%: Scaling Transfection Efficiency. 19:57 — Mass Production: Automated Cassettes for Stem Cells. 24:57 — Slashed Costs: Disrupting the $10M Treatment Price Tag. 29:58 — Retrovirus Danger: Preventing Toxic Contamination. 35:01 — Japan’s Law: Safety Testing & Rejuvenation Services. 39:58 — Next-Gen Immune Therapy: iPSCs vs Cancer & Aging. 44:59 — The In-Vivo Reprogramming Risk: Why It Fails. 49:59 — Infinite Cellular Supply: Pluripotency’s Power. 54:57 — Beyond Reprogramming: Solving the Extracellular Matrix.

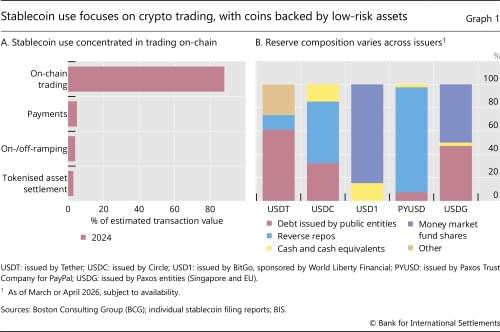

Digital innovation is transforming finance. It creates opportunities, but also poses challenges and raises the question on how to preserve trust in money.

The lithium-ion battery is the beating heart of the modern world. It powers eight billion mobile phones, hundreds of millions of laptops and rapidly growing fleets of electric cars and energy-storage banks. But there’s a new contender breaking into the battery market.

Batteries based on sodium promise to be cheaper, safer and much more environmentally friendly than lithium-ion cells. And this year could mark the start of the sodium era.

In April, Chinese firm CATL — the world’s largest battery producer — announced that it will start mass-producing sodium-ion batteries before the end of 2026. CATL, which is headquartered in Ningde, added that it had signed deals to sell the batteries both to a car manufacturer and to a provider of energy-storage stations for electricity grids.

A threat actor has published hundreds of fake GitHub repositories impersonating legitimate software and security projects to distribute infostealer malware.

The campaign drew traffic from search results for security products, cryptocurrency services, financial tools, developer utilities, secure email providers, macOS utilities, and gaming software.

The malware collects data from more than 19 web browsers, steals info from 32 cryptocurrency wallets, and exfiltrates sensitive details from messaging and social media apps.