A cryptocurrency entrepreneur launched a blockchain religion. Absolutely no one is surprised.

I get this question a lot. Today, I was asked to write an answer at Quora.com, a Q&A web site at which I am the local cryptocurrency expert. It’s time to address this issue here at Lifeboat.

I have many PCs laying around my home and office.

Some are current models with fast Intel CPUs. Can

I mine Bitcoin to make a little money on the side?

Other answers focus on the cost of electricity, the number of hashes or teraflops achieved by a computer CPU or the size of the current Bitcoin reward. But, you needn’t dig into any of these details to understand this answer.

You can find the mining software to mine Bitcoin or any other coin on any equipment. Even a phone or wristwatch. But, don’t expect to make money. Mining Bitcoin with an x86 CPU (Core or Pentium equivalent) is never cost effective—not even when Bitcoin was trading at nearly $20,000. A computer with a fast $1500 graphics card will bring you closer to profitability, but not by much.

The problem isn’t that an Intel or AMD processor is too weak to mine for Bitcoin. It’s just as powerful as it was in the early days of Bitcoin. Rather, the problem is that the mining game is a constantly evolving competition. Miners with the fastest hardware and the cheapest power are chasing a shrinking pool of rewards.

The problem arises from a combination of things:

Of course, with Bitcoin generally rising in value (over the long term), this provides continued incentive to mine. It is the only thing that makes this game worthwhile to the individuals who participate.

So, while it is not impossible to profit by mining on a personal computer, if you don’t have very cheap power, the very latest specialized mining rigs, and the skills to constantly tweak your configuration—then your best bet is to join a reputable mining pool. Take your fraction of the mining rewards and let them take a small cut. Cash out frequently, so that you are not locked into their ability to resist hacking or remain solvent.

Related: Largest US operation mines 0.4% of daily Bitcoin rewards. Listen to the owner describe the effiiency of his ASIC processors and the enormous capacity he is adding. This will not produce more Bitcoin. The total reward rate is fixed and falling every 4 years. His build out will consume a massive amount of electricity, but it will only grab share from other miners—and encourage them to increase consuption just to keep up.

* Several readers have pointed out that they have access to “free power” in their office — or more typically, in a college dormitory. While this may be ‘free’ to the student or employee, it is most certainly not free. In the United States, even the most efficient mining, results in a 20 or 30% return on electric cost—and with the added cost of constant equipment updates. This is not the case for personal computers. They are sorely unprofitable…

So, for example, if you have 20 Intel computers cooking for 24 hours each day, you might receive $115 rewards at the end of a year, along with an electric bill for $3500. Long before this happens, you will have tripped the circuit breaker in your dorm room or received an unpleasant memo from your boss’s boss.

Bitcoin mining farms —

This is what you are up against. Even the amateur mining operations depicted in the bottom row require access to very cheap electricity, the latest processors and the skill to expertly maintain hardware, software and the real-time, mining decision-process.

Philip Raymond co-chairs CRYPSA, hosts the New York Bitcoin Event and is keynote speaker at Cryptocurrency Conferences. He sits on the New Money Systems board of Lifeboat Foundation. Book a presentation or consulting engagement.

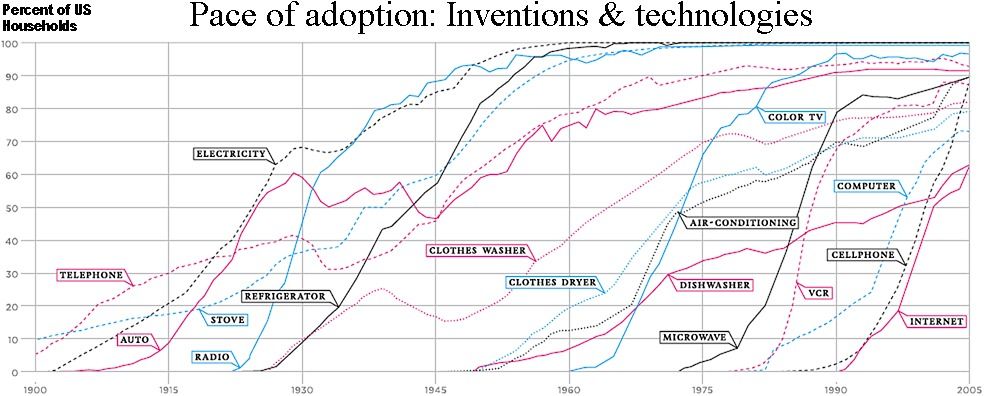

Early adopters, speculators and Geeks are never sufficient to bring a new paradigm to market. Mass appeal and adoption of a mechanism that requires education and a change of behavior is never ‘fait accompli’—until it reaches a tipping point. Once at the tipping point, it can go viral without a structured PR campaign and with risks tied only to technology and scalability.

The question was asked of me as columnist at Quora.com: Will governments eventually ‘approve’ of cryptocurrency? First let’s agree on terminology…

A blockchain-based cryptocurrency that is open source, permissionless, capped, fast, frictionless, with a transparent history—and without proprietary or licensing restrictions is good for everyone. It is good for consumers; good for business; and it is even good for government.

Of course, politicians around the world are not quick to realize this. It will take years of experience, education, and policy experimentation.

Many pundits and analysts have the impression that shifting to cryptocurrency—not just as a payment instrument, but as the money itself—will never be supported by national governments. A popular misconception suggests that a cryptocurrency based economy has these undesirable traits:

Over time, perceptions will change, because only the last entry is true. Adoption of cryptocurrency puts trust into math rather than the whims of transient politicians. It helps governments avoid the trap of hoisting debt on future generations or making promises to creditors that they cannot keep—Yet, it does not lead to the maladies on this list.

But, what about that last item? Does an open source currency cause a nation to lose control over its own monetary policy? Yes! But it is not bad! Crypto cannot be printed, gamed or manipulated. Despite perception, it is remarkably resistant to loss or theft. Early hacks and fiascos were enabled by a lack of standards, tools and education. As with any new technology—especially one that changes practices or institutions—adoption of radical processes goes hand-in-hand with gradual understanding and acceptance of benefits.

How Does Crypto Help Governments?

Adopting/accepting a national (or international) cryptocurrency is a terrific way for governments to earn the respect and trust of citizens, businesses, consumers and especially creditors. There is no more reason for governments to control their money supply than there is for them to control communication networks, space travel or package delivery services.

You may not agree that cryptocurrency is good for government, and so I expand on the topic here. But your question doesn’t ask if it is good, it asks if governments are likely to approve.

Yes. Eventually…

First, a few forward thinking countries like Iceland, Japan or UAE will spearhead adoption of a true, permissionless cryptocurrency (or at least recognize it as legal tender) . Later, ‘stress-economies’ will join the party: These are countries that need to control either rampant inflation, a reluctance to tax citizens, treasury mismanagement or massive international debt. A solution to these problems requires restoration of public trust. I wouldn’t be surprised to see Greece, Zimbabwe, Venezuela or Argentina in the mix.*

Eventually, G7 countries will tread into a growing ocean. Not now; but in 5 or 8 years. The conditions are not yet right. It requires further vetting by early adopters, continued development, education and then popular consumer adoption. But all of these things are inevitable. Eventually, governments will recognize that a capped, trusted, transparent, math-based money is far better for all stakeholders than money based on intrinsic value, promise-of-redemption or force.

* We are not discussing countries that plan to create their own cryptocurrency. None of these plans involve a coin that is open source, permissionless, decentralized and capped. They are simply replacing paper with a national debit card. But it is not crypto.

Philip Raymond co-chairs CRYPSA, hosts the New York Bitcoin Event and is keynote speaker at Cryptocurrency Conferences. He sits on the New Money Systems board of Lifeboat Foundation. Book a presentation or consulting engagement.

I love clearing the air with a single dismissive answer to a seemingly complex question. Short, dismissive retorts are definitive, but arrogant. It reminds readers that I am sometimes a smart a*ss.

Is technical analysis a reasoned approach for

investors to predict future value of an asset?

In a word, the answer is “Hell No!”. (Actually, that’s two words. Feel free to drop the adjective). Although many technical analysts earnestly believe their craft, the approach has no value and does not hold up to a fundamental (aka: facts-based) approach.

One word arrogance comes with an obligation to substantiate—and, so, let’s begin with examples of each approach.

Investment advisors often classify their approach to studying an equity, instrument or market as either a fundamental or technical. For example…

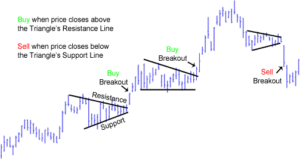

Do you see the difference? Fundamental analysis is rooted in SWOT: Study strengths, weaknesses, opportunities, and threats. Technical analysis dismisses all of that. If technical jargon and approach sound a bit like a Gypsy fortune teller, that’s because it is exactly that! It is not rooted in revenue and market realities. Even if an analyst or advisor is earnest, the approach is complete hokum.

I have researched, invested, consulted and been an economic columnist for years. I have also made my mark in the blockchain space. But until now, I have hesitated to call out technical charts and advisors for what they are…

Have you noticed that analysts who produce technical charts make their income by working for someone? Why don’t they make a living from their incredible ability to recognize patterns and extrapolate trends? This rhetorical question has a startlingly simple answer: Every random walk appears to have patterns. The wiring of our brain guarantees that anyone can find patterns in historical data. But the constant analysis of patterns by countless investors guarantees that the next pattern will be unrelated to the last ones. That’s why short term movement is called a “random walk”. Behaviorists and neuroscientists recognize that apparent relationships of past trends can only be correlated to future patterns in the context of historical analysis (i.e. after it has occurred).

Decisions based on a technical analysis—instead of solid research into fundamentals—is the sign of an inexperienced or gullible investor. Some advisors who cite technical charts know this. Technicals have no correlation to long term appreciation, asset quality or risks. They only point to short term possibilities.

The problem with focusing on short-term movement is that you will certainly lose to insiders, lightning-fast program traders, built in arbitrage mechanisms and every unexpected good news/bad news bulletin.

If you seek to build a profit in the long run, then do your research up front, enter gradually, and hold for the long term. Of course, you should periodically reevaluate your positions and react to significant news events from trusted sources. But you should not anguish over your portfolio every day or even every month.

Finally, if someone tries to dazzle you with charts of recent performance and talk of a “resistance level” or support trends, smile and nod in approval—but don’t dare fall for the Ouija board. Send them to me. I will straighten them out.

Who says so? Does the author have credentials?

I originally wrote this article for another publication. Readers challenged my credentials by pointing out that I am not a academic economist, investment broker or financial advisor. That’s true…

I am not an academic economist, but I have certainly been recognized as a practical economist. Beyond investor, and business columnist, I have been keynote speaker at global economic summits. I am on the New Money Systems Board at Lifeboat Foundation, and my career is centered around research and public presentations about money supply, government policy and blockchain based currencies. I have advised members of president Obama’s council of economic advisors and I have recently been named Top Writer in Economics by Quora.

I am not an academic economist, but I have certainly been recognized as a practical economist. Beyond investor, and business columnist, I have been keynote speaker at global economic summits. I am on the New Money Systems Board at Lifeboat Foundation, and my career is centered around research and public presentations about money supply, government policy and blockchain based currencies. I have advised members of president Obama’s council of economic advisors and I have recently been named Top Writer in Economics by Quora.

Does all of this qualify me to make dismissive conclusions about technical analysis? That’s up to you! This Lifeboat article is an opinion. My opinion is dressed as authoritative fact, because I have been around this block many times. I know the score.

Related:

Philip Raymond co-chairs CRYPSA, hosts the Bitcoin Event and is keynote speaker at Cryptocurrency Conferences. He sits on the Lifeboat New Money Systems board. Book a presentation or consulting engagement.

ASUS is moving further into the cryptocurrency hardware market with a motherboard that can support up to 20 graphics cards, which are typically used for mining. The H370 Mining Master uses PCIe-over-USB ports for what ASUS says is sturdier, simpler connectivity than other mining-focused motherboards.

You can manage each port and graphics card with on-board diagnostics. One feature scans your system when you boot up to determine the status of each port, while there are onboard LEDs that signify a problem with components such as memory or the processor (there’s space for an Intel 8th-gen Core CPU). ASUS has added some other features to optimize mining as well.

The H370 Mining Master follows last year’s B250 Mining Expert, which had room for 19 CPUs via PCIe ports. ASUS says that board had far more sales than it expected, which prompted the company to keep traveling down the crypto road and evolve its mining-tailored motherboards. The latest board will ship later this year, though ASUS has yet to announce pricing. You might need to fork over several Ethereum coins to buy enough graphics cards for all those spaces, though.

Other than the United States, 5 U.S. territories and 12 sovereign nations use the US dollar as their legal currency. (Note that Micronesia covers six sovereign countries).

Additionally, I have traveled to island nations and some countries in Asia and Pacific that peg their currency to the US dollar. In these regions, citizens accept US dollars interchangeably with their own national currency, and their governments don’t seem to discourage or prosecute such transactions.

What gives value to paper?

Around 350 BC, Aristotle worked for the Greek council, trying to get farmers, weavers, chariot makers and tradesman to use government issued currency for the exchange of goods and services, rather than bartering with neighbors. This would not only facilitate taxation and public works, but it would help farmers to store and forward their wealth, instead of seeing their assets perish with each change of season.

He reflected on what makes a currency trusted and functional. He felt that one critical trait was “intrinsic value”. Today, most economists interpret this phrase as a currency having inherent or self-contained value. That is, it mustn’t be paper nor even a promise of redemption (for example, a picture of Caesar). And it mustn’t rely on the ‘good faith and credit’ of citizens. After all, nations are subject to the whims of transient politicians and any economy can collapse because of war, drought or over-spending. Rather, the money must be made from something of useful and dense value. For example, it could be gold, silver or some useful thing, like chocolate, coveted jewelry or a tool.

Today, money is no longer backed by gold or even a government promise of redemption (offering to exchange dollars for gold, grain, goats or land). For developed nations, this backing—a method of establishing intrinsic value—ended between 1971~1973, when President Richard Nixon dissolved the Bretton Woods Agreement and withdrew the promise of a conversion guaranty.

Instead, today, the value of national currencies floats in response to supply and demand.

Supply and demand is a natural economic mechanism, and for fluid and widely distributed commodities, it can be an elegant solution to the problem of establishing value, function and durability—but only if the supply is capped or very tightly regulated and the issuer is trusted by individuals, organizations and nations that quote prices, save or trade with the currency.

Unfortunately, this is not the case for any national currency across the world.

Today, it’s all about trust—Trust in the ability of a country to return the goods and services that were bought by their people and trust in their government to avoid printing more money, which depreciates savings, redistributes wealth, and cheats creditors through the insipid dilution of inflation.

Whenever a government prints money, it reneges on debt and breeches the trust of creditors.

Why would any country substitute the currency of another country?

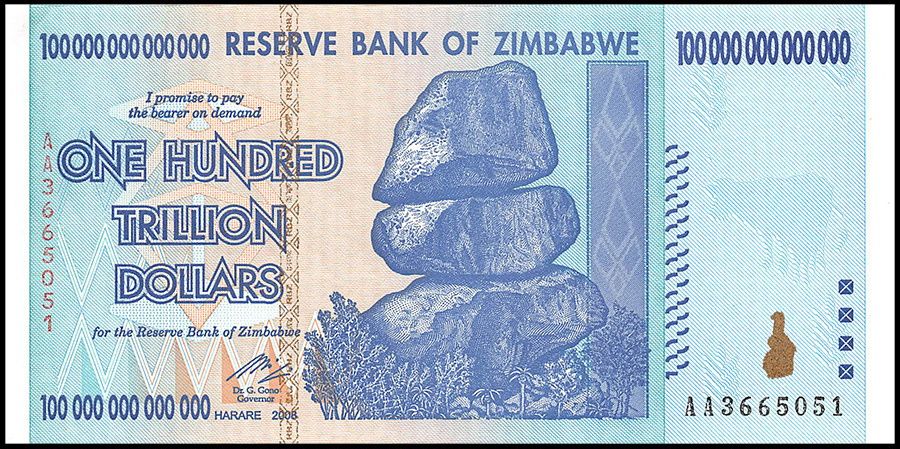

One need only look at this Zimbabwe money to understand why an independent nation might substitute the US dollar as legal tender. The same has happened to Argentina, Greece, Venezuela and Germany between the wars.

It was withdrawn from circulation in 2008. At the time, it was worth US 40¢ (40 cents). Today, Zimbabwe uses the US dollar as its legal currency, because its spending value is stable relative to monies issued African central banks. That is, the citizens trust the US dollar to resist inflation—and so they use it to store and trade their hard-earned wealth.

Is Adoption of the US Dollar growing around the world?

The days of our friends and enemies trusting the dollar or even using it to negotiate large international trades is gradually coming to an end. This is changing, because:

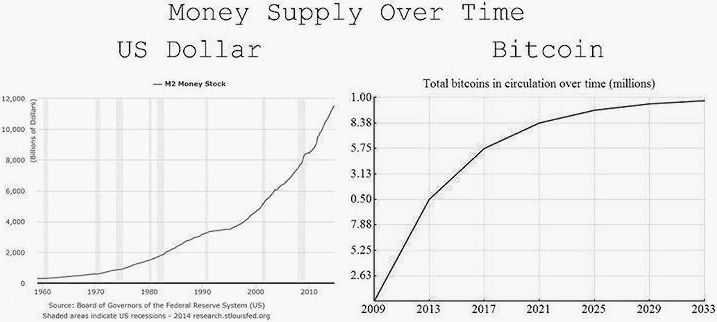

1. Bitcoin is gradually displacing the dollar as the world’s reserve currency. Even though it is slow to gain traction as a commercial and consumer payment instrument, it has all the components of an ideal currency for large international quotation, exchange and settlement.

The fundamental reason for the gradual trust in Bitcoin is illustrated by these graphs. Bitcoin is a capped commodity backed by a robust 2-sided network. Understanding and trust in its distributed consensus mechanism is growing. It cannot be manipulated by transient politicians. Nations that use it for significant transactions cannot be cheated when their trading partner or a 3rd party prints money to cover their own shortfall. It is an ideal reserve settlement instrument.

2. In recent decades, the dollar is built on debt rather than domestic output, a trade surplus, or high quality credit. This creates the potential for a collapse, if US citizens or creditor nations begin to doubt the likelihood of the United States reversing its slumping exports and staggering trade imbalance.

3. In recent years, the United States has lost gravitas in world forums due to the projection of power beyond its borders without a clear mandate or international support, and its recent lack of leadership in issues like the environment, trade accords and arbitrating regional peace agreements. This impression—along with the erratic statements and behavior of U.S. politicians causes both allies and enemies to seek an alternate reserve currency. Why so? …

A reserve currency is an international quotation and settlement instrument—even when the United States is not a party to a sale or transaction, and even if one or both parties is not a US ally. Many countries, banks and producers (of oil, food, military gear, etc) do not desire or appreciate the tremendous side-benefit that accrues to USA.

In effect, when you adopt the currency of one nation as the reserve currency for others, you grant credit to that country, without collateral. You allow them to print money without substantive backing, guarantees or even a balance of trade that makes it likely you will be repaid without the dilution of inflation.

Ellery Davies co-chairs CRYPSA, hosts the New York Bitcoin Event and is keynote speaker at Cryptocurrency Conferences. He sits on the New Money Systems board of Lifeboat Foundation. Book a presentation or consulting engagement.

The Marshall Islands made its own cryptocurrency, doing away with the US dollar. The government has signed the change into law, making the “sovereign” its new official cryptocurrency, as spotted by CNBC Africa cryptocurrency trader host Ran Neuner on Twitter yesterday.

The bill was signed into effect on March 1st, but the news is making waves again this week. The Marshall Islands’ population is 53,066, so the change doesn’t affect many, but it is significant for citizens of the islands because banks and credit card companies will need to begin accepting it. With the recent change, US dollars are still likely to be accepted on the Marshall Islands — the sovereign will just be considered the nation’s official legal tender.

In February, top officials from the Marshall Islands confirmed that the Pacific republic would issue its own cryptocurrency to be circulated as legal tender. The digital coin also received approval from the country’s parliament. “As a country, we reserve the right to issue a currency in whatever form it is, whether in digital or fiat form,” said David Paul, minister-in-assistance to the president of the Marshall Islands, to Reuters at the time.

{kind=link}

{kind=link}

{kind=link}