Blockchain can’t stop unauthorized access, but it could help lessen the damage.

Category: bitcoin – Page 70

Blockchain Art Exhibitions Explore the Bitcoin Technology’s Future — By Steven Norton | The Wall Street Journal

“That contemporary artists are exploring blockchain further suggests the technology has reached a level of cultural significance beyond bitcoin’s initial hype.”

Why Bitcoin is and isn’t like the Internet — By Joichi Ito | LinkedIn

“In the post that follows I’m trying to develop what I see to be strong analogues to another crucial period/turning point in the history of technology, but like all such comparisons, the differences are as illuminating as the similarities.”

UAE considers blockchain technology to prevent global trade of ‘conflict diamonds’

New methods to counter attack fraud.

“We have introduced the possibility of using blockchain technology to create a seamless and continued global process for the KP certification scheme,” he said.

Blockchain is one of the most significant elements of the revolution in financial technology – fintech – that has been enthusiastically adopted by the UAE. Both Dubai and Abu Dhabi are setting up centres of excellence in fintech.

Mr bin Sulayem has already had meetings with Dubai’s Blockchain Council and is working on a pilot project that would use the technology to monitor KP statistics.

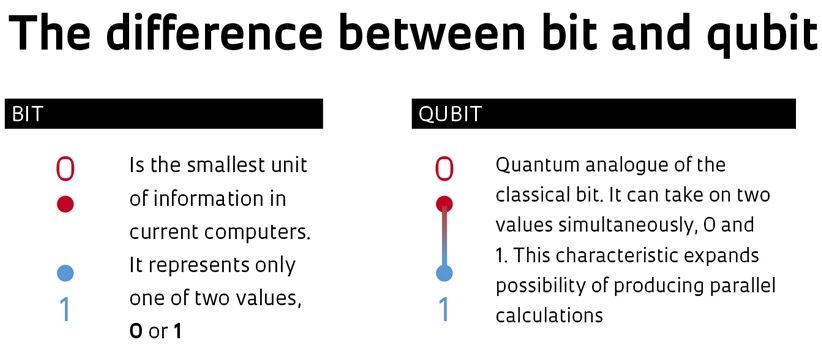

Quantum computing and cryptocurrencies: Are Steemit and bitcoin safe?

Article repeats a lot of the knowns on QC such as bit v. Qubit; and finally provides some good info on pros and cons of Bitcoin and Lamport signatures technique with QC. However, the author didn’t seem to mention any of the work that D-Wave for example is doing with Block chaining. Also, I saw no mention of the work by Oxford on the logic gate which improve both the information processing performance and the security of information transmissions.

In a classical computer bits are used that can either be 0 or 1. In a quantum computer these bits are replaced with Qubits (quantum bits). These Qubits can be 0 or 1, or both at the same time. This is caused by a phenomenon in the quantum realm called superposition. At scales the size of an atom and small molecules, the spin of particles is not determined until it is observed. A pair of Qubits can be in any quantum superposition of 4 states, and three Qubits in any superposition of 8 states. In general, a quantum computer with n Qubits can be in a superposition of up to 2^n different states simultaneously (this compares to a normal computer that can only be in one of these 2^n states at any one time). Because of this, a quantum computer is able to perform computations at the same time, while classical computers perform computations one at a time.

{kind=link}

This effectively means that the computing power grows exponentially for each Qubit you add to the system. A quantum computer will be able to make really difficult calculations all the classical computers in the world together would not be able to do before the end of times, in a relatively short amount of time. This opens to world of computing to be able to perform amazingly complex calculations, such as weather or large scale quantum mechanics, with extremely high precision. Unfortunatly, it will also be great at cracking certain types of cryptography.

In Blockchain We Trust

I was a guest on the Robot Overlordz podcast again recently, and was asked about my post on Medium for KnowledgeWorks called “Preparing for Hybrid Schools and Jobs.” The conversation with Mike and Matt took some interesting turns, as always, and they got me thinking about some really important questions when it comes to blockchain and society, namely: assuming blockchain lives up to it’s reputation as a ‘truth machine,’ as I refer to it in my post, or a ‘revolution,’ as the Tapscotts say, why is there now a need for a revolutionary technology to enhance trust?

Although blockchain has captured the attention of the financial, management consulting and consumer goods industries, it hasn’t quite taken hold in education yet. KnowledgeWorks has published a fantastic report on the possibilities. I suggest in my post that the rise of hybrid jobs will generate support for hybrid schooling, and blockchain may be the technology that is best suited to track and communicate qualifications. The World Economic Forum said it best: “Farewell Job Title, Hello Skill Set.” If we are to be evaluated on our skills and experience, we must have some reliable way of guarding and transmitting that information.

But why is it that we need to enhance trust among students and teachers, employees and employers? I think that the facts that college students (some who didn’t even graduate) owe massive student loans, though worker’s wages have gone stagnant, play into this tension. How can students trust schools to provide the education they need, considering the high cost and the gamble that it may never really be recouped?

We are beginning to see slight signals that things are changing, at least a little, on the remuneration side, and it’s possible that a truth machine could help restore trust to hierarchical relationships (student/university and employee/employer) that are extremely out of balance. But what is at risk in assuming a technology can reverse human corruption?